UP主: 封面: 简介:https://markus.scholar.princeton.edu/classes/eco529-macro-money-and-international-financePrinceton博士课程,面向研究宏观经济、宏观金融、货币经济金融、国际金融的...

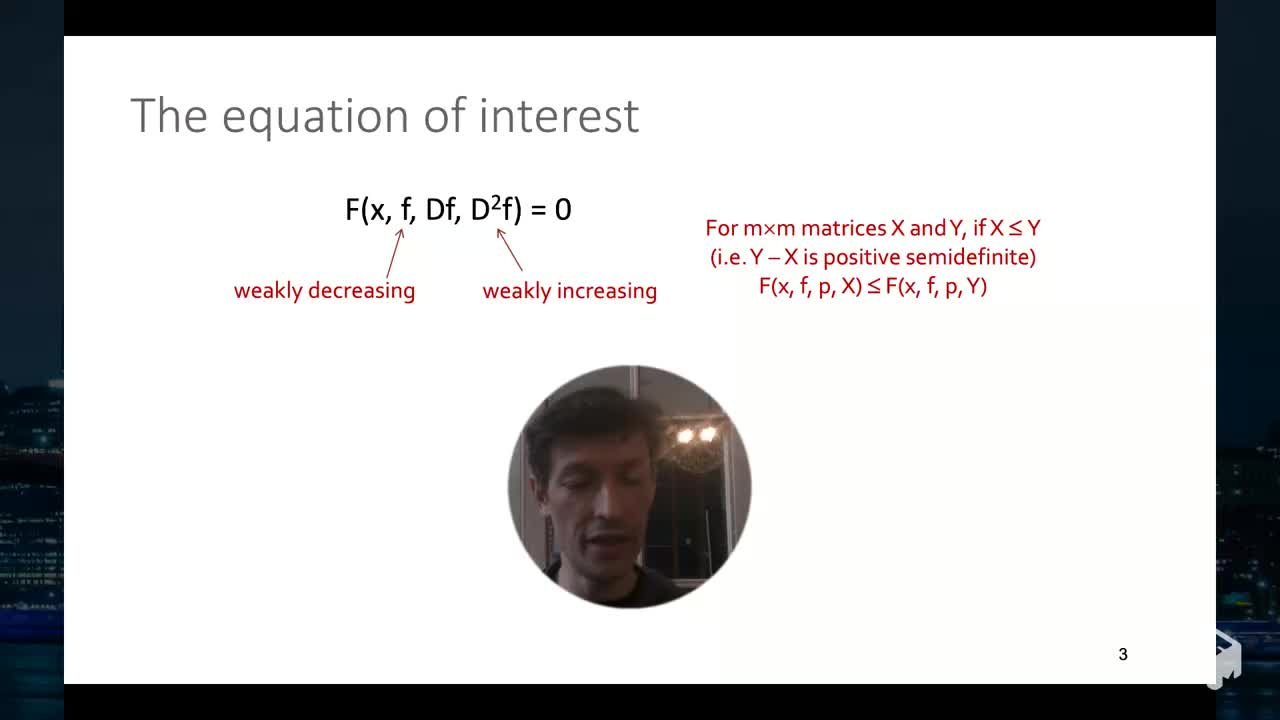

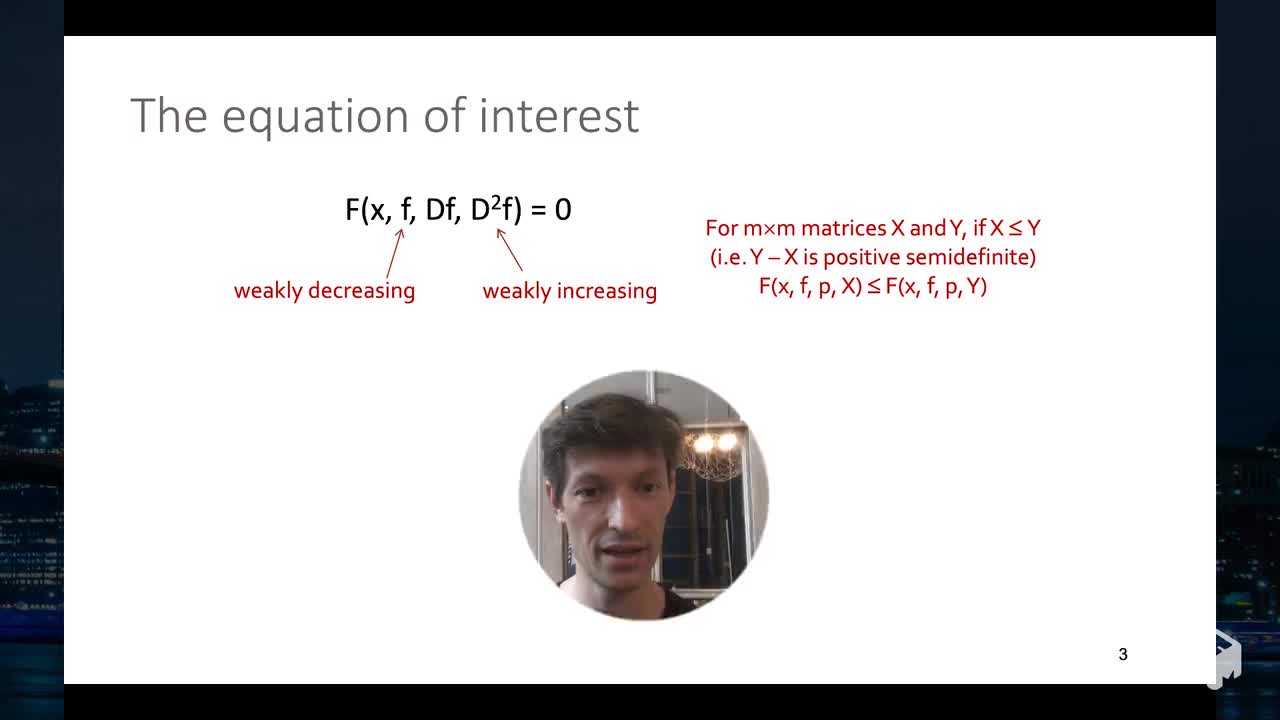

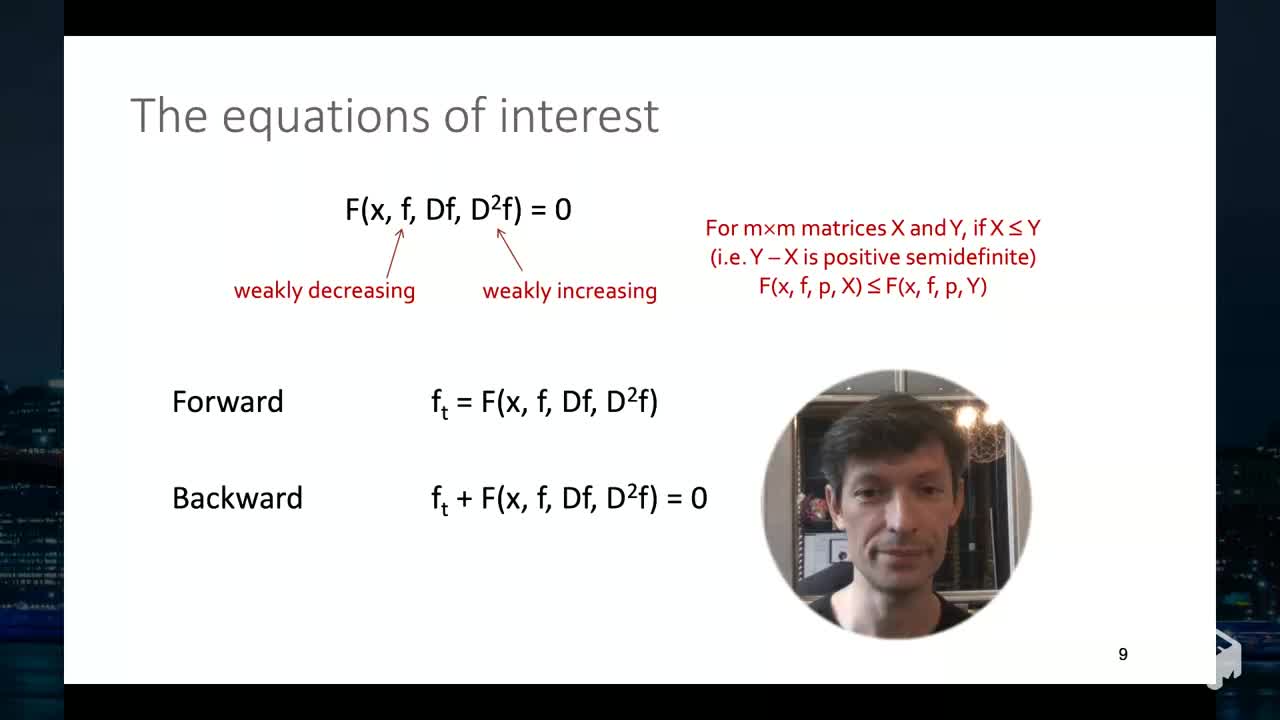

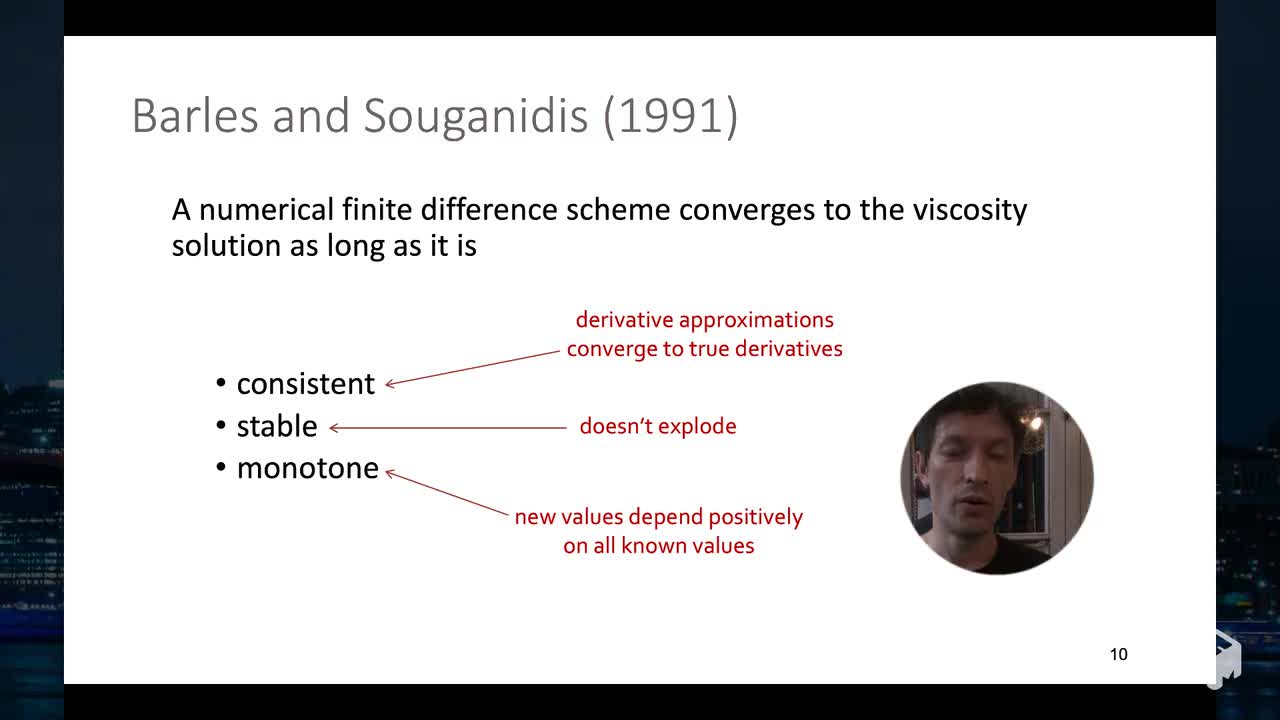

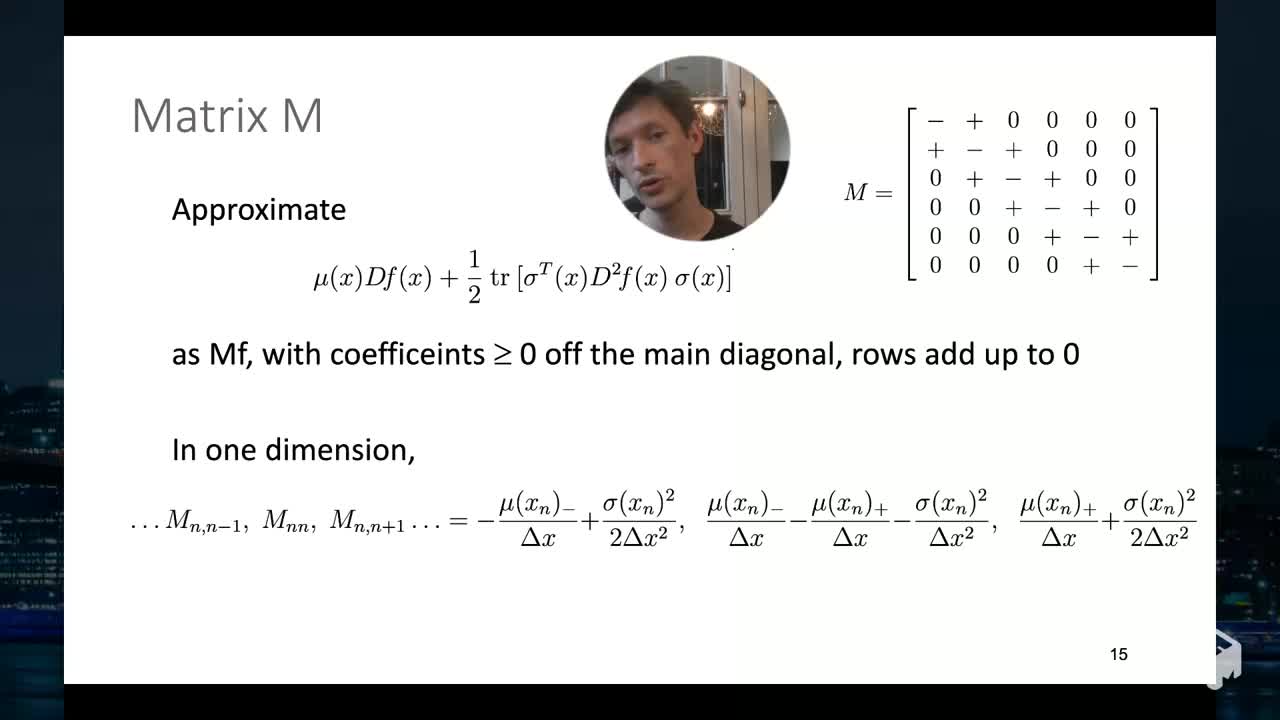

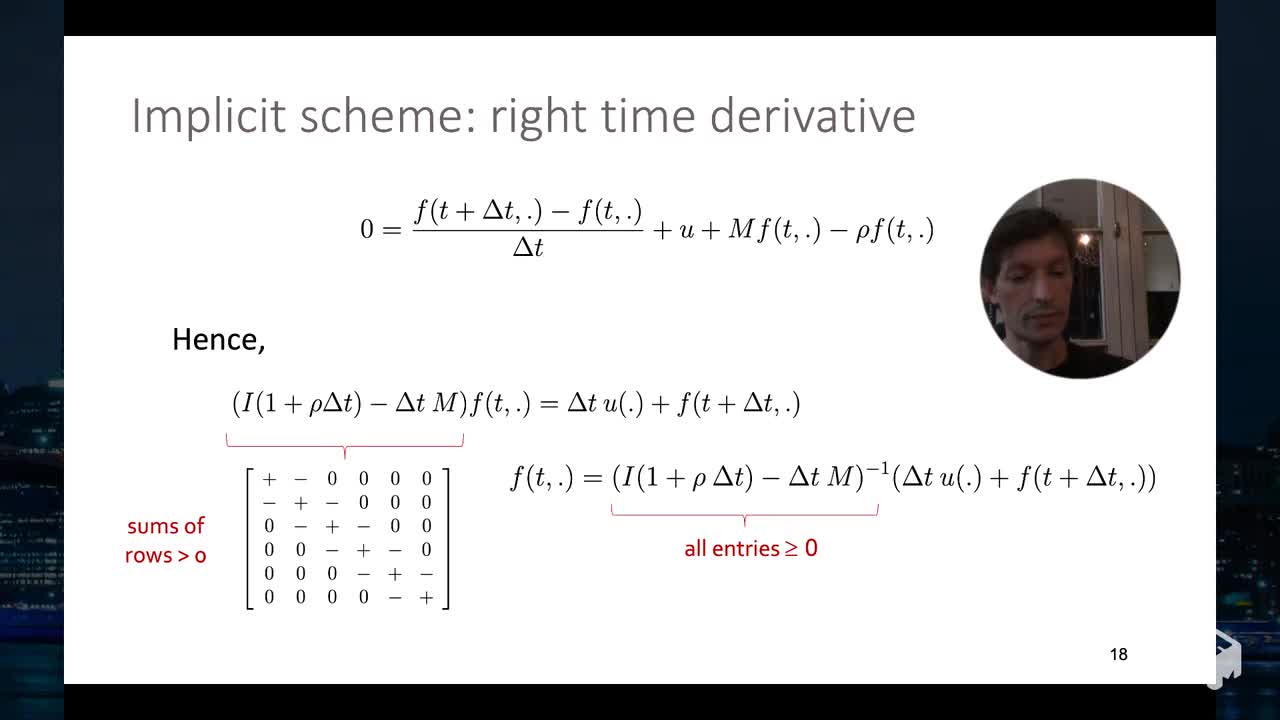

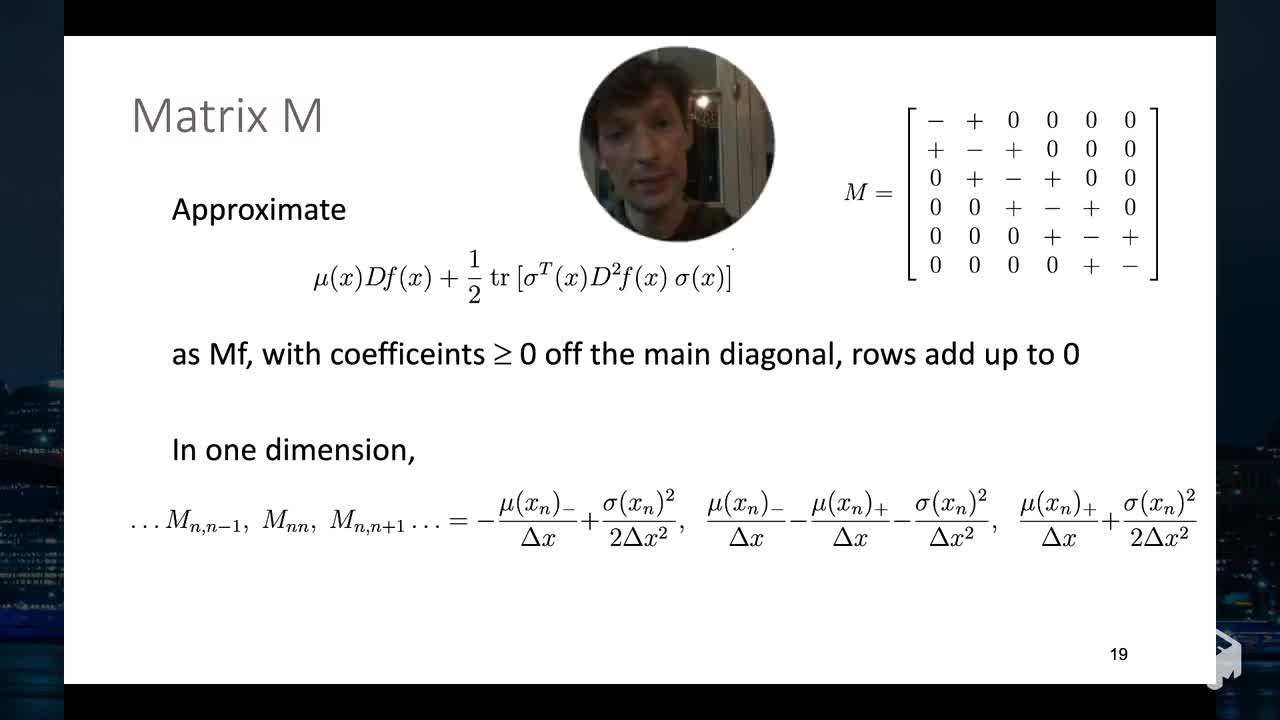

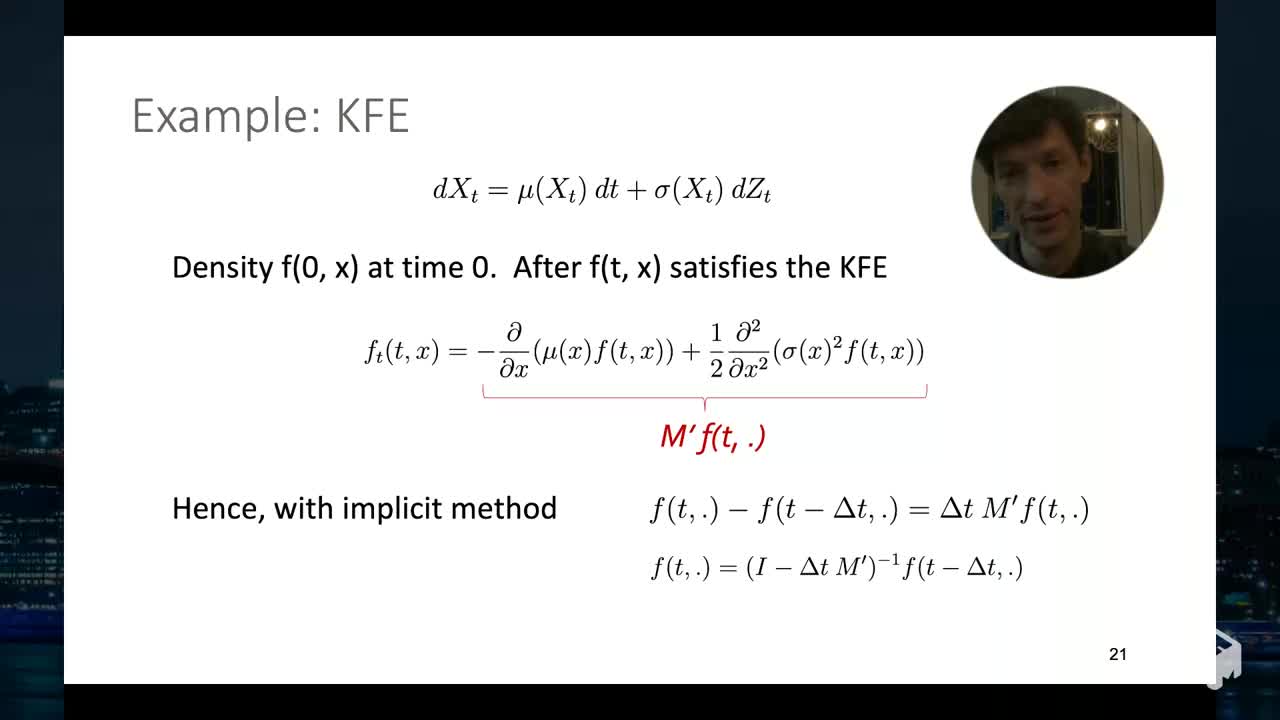

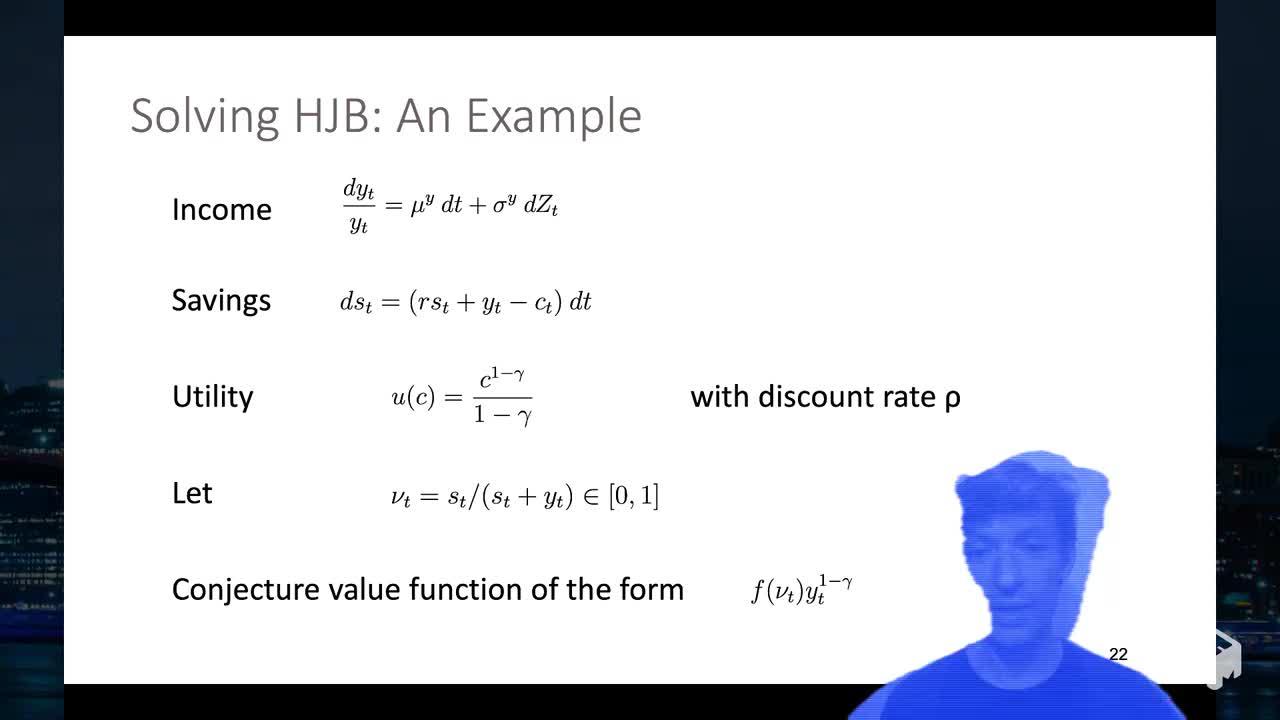

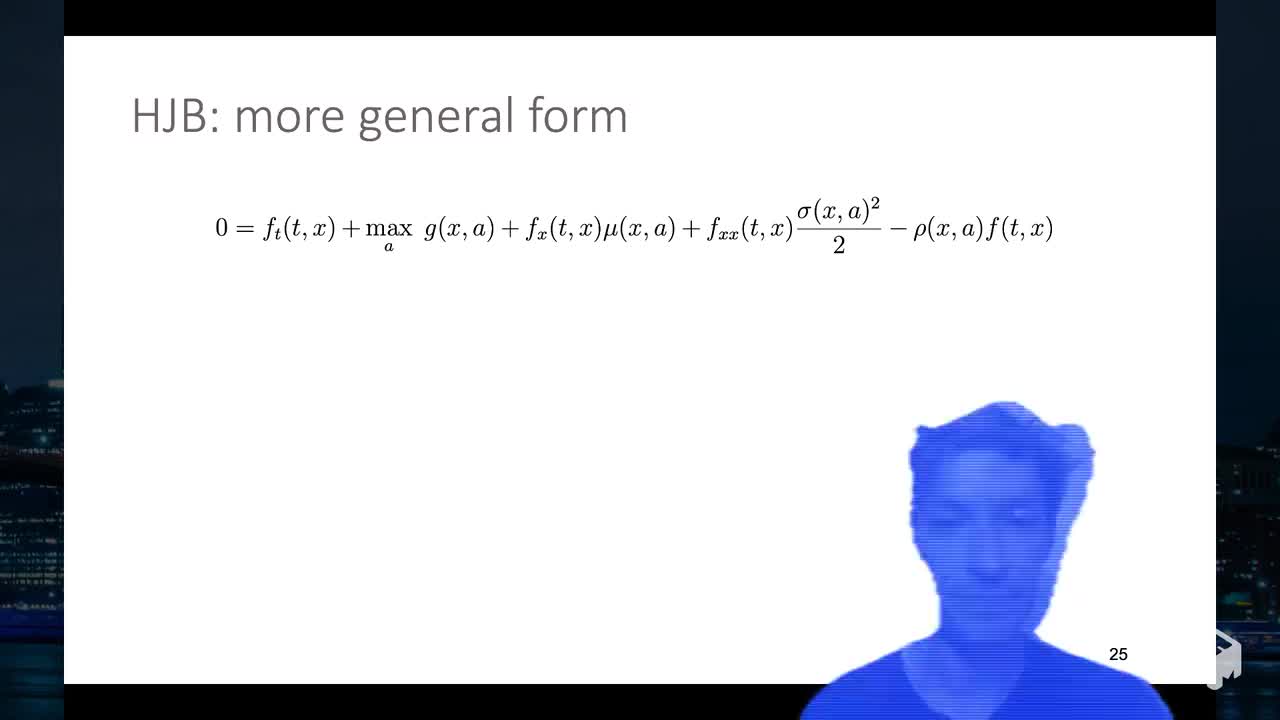

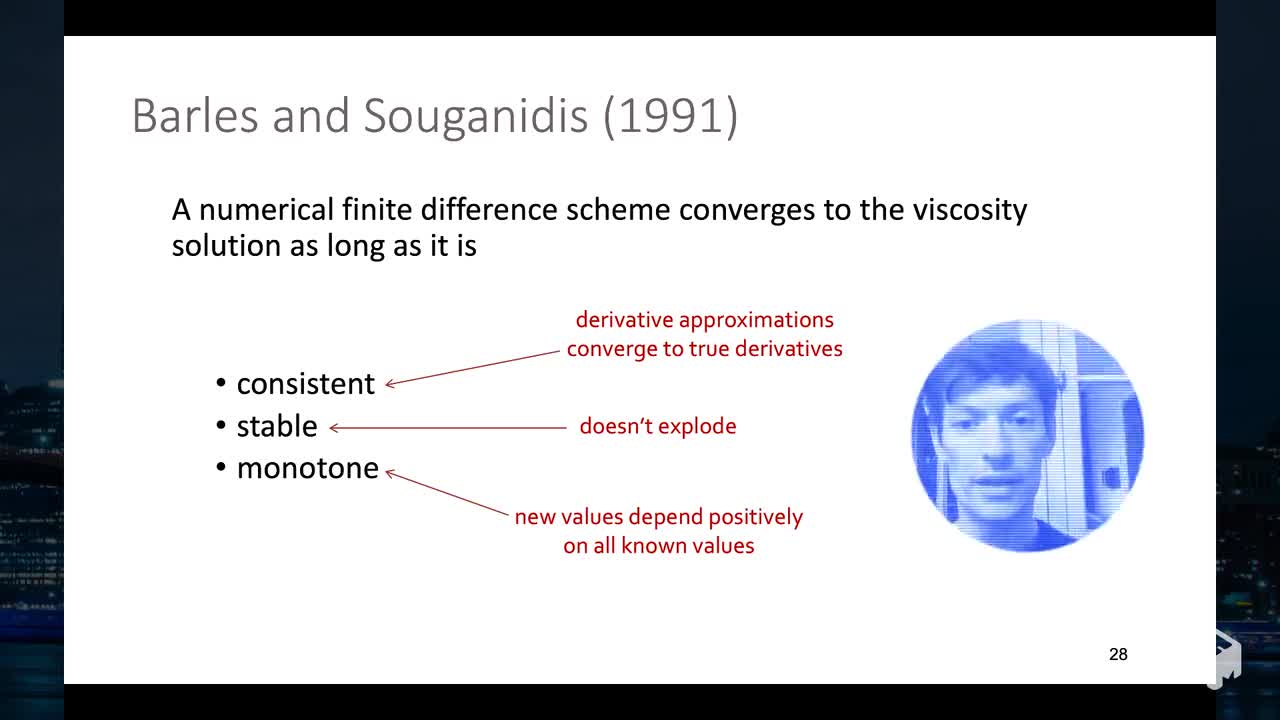

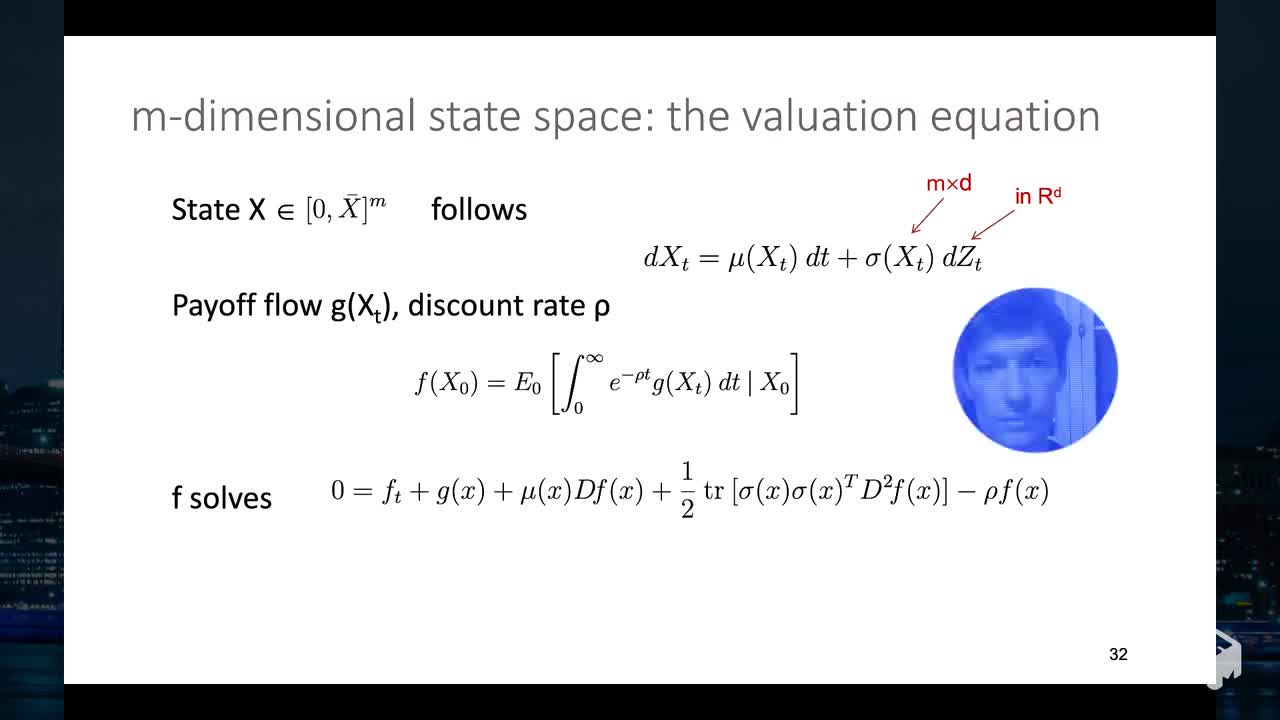

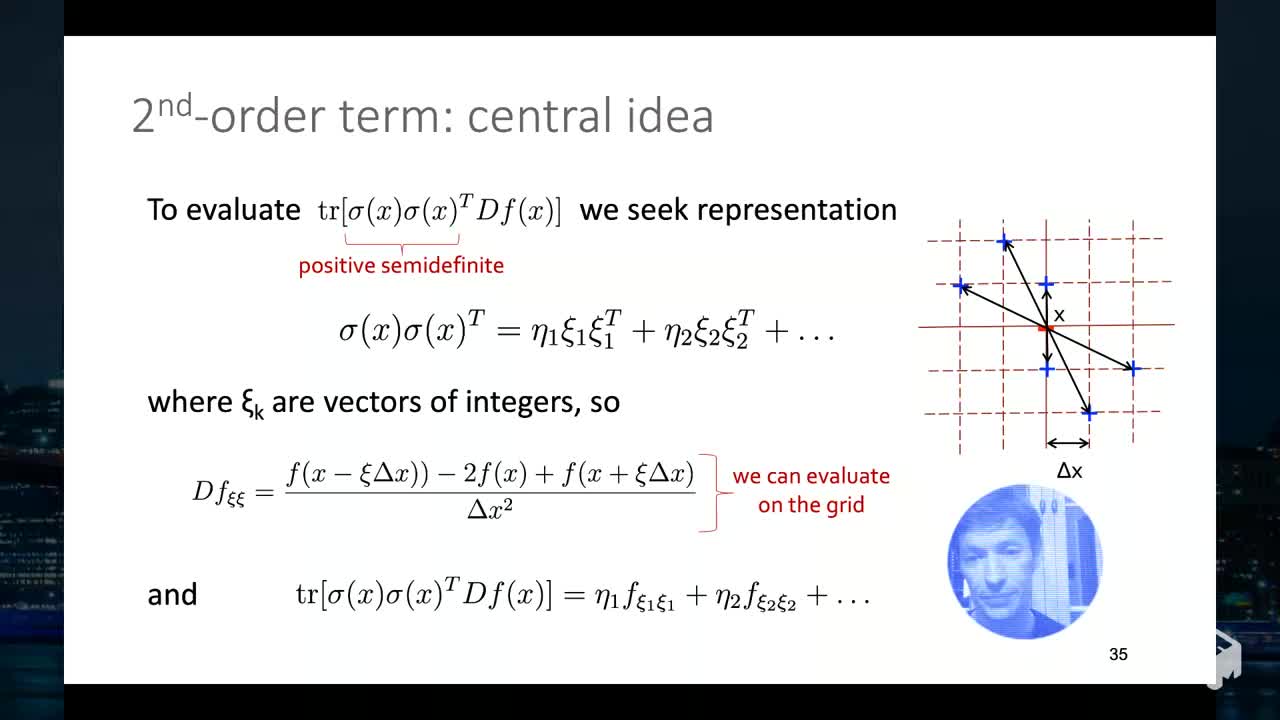

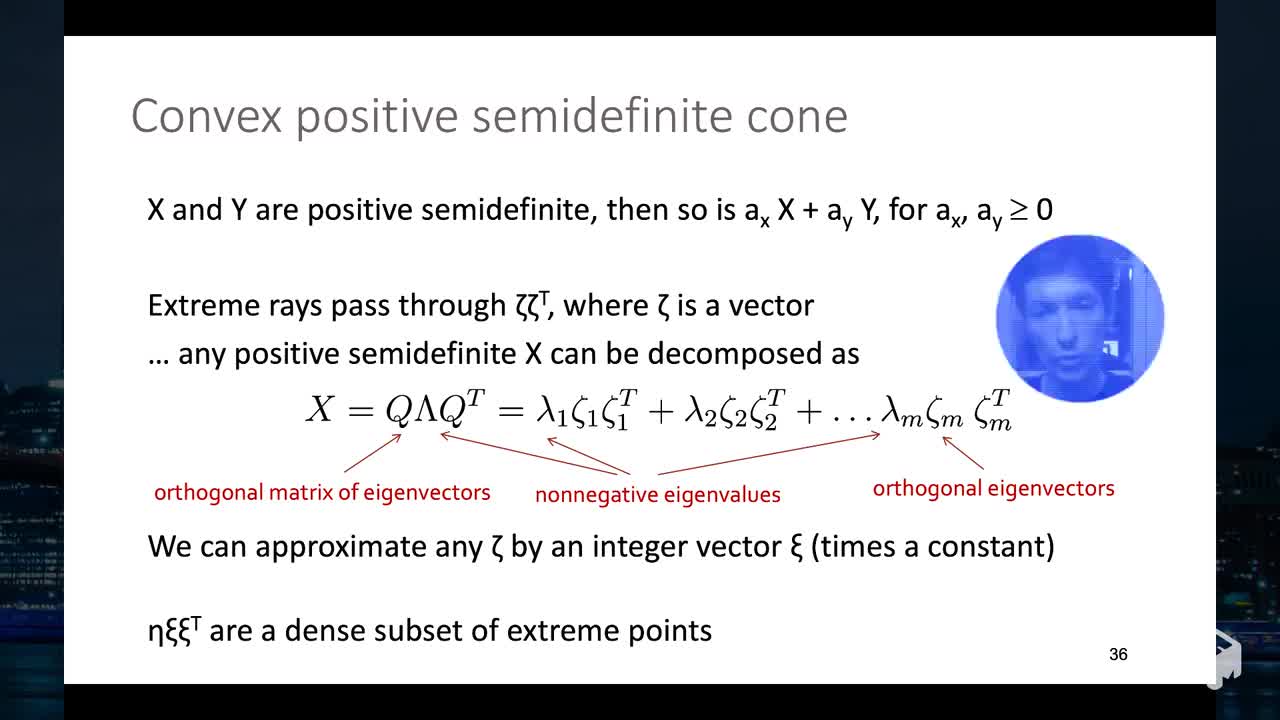

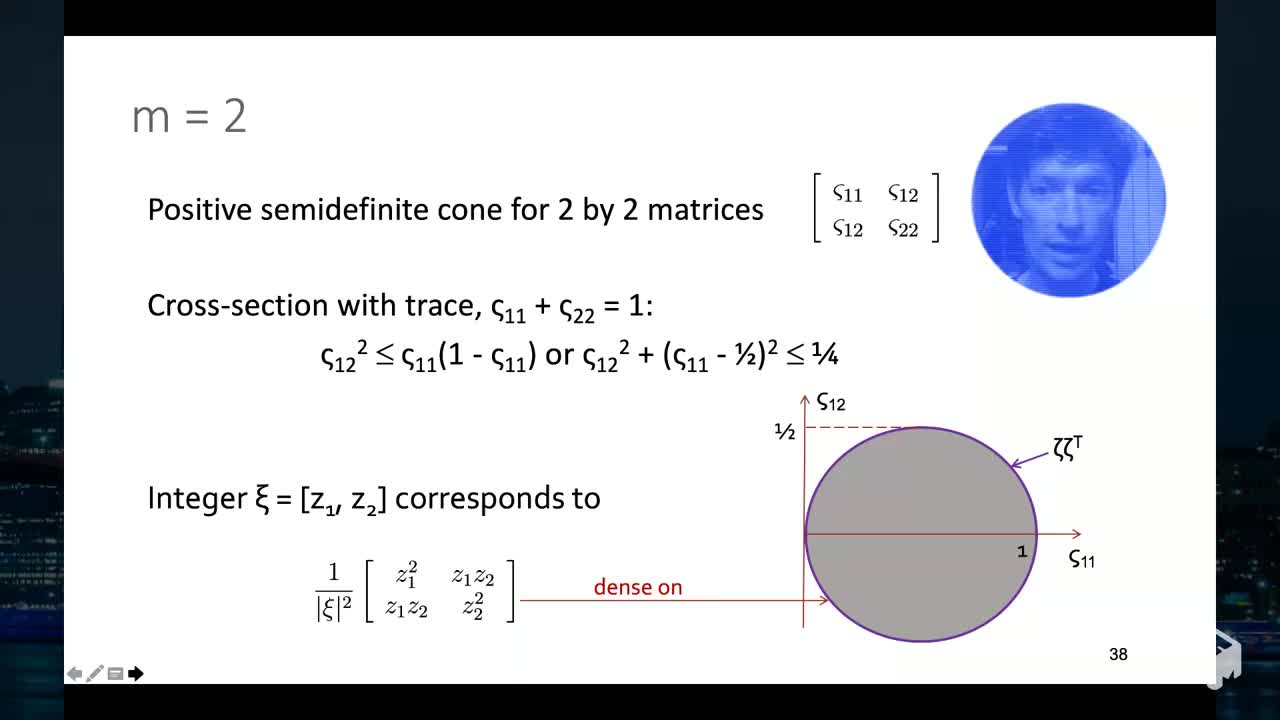

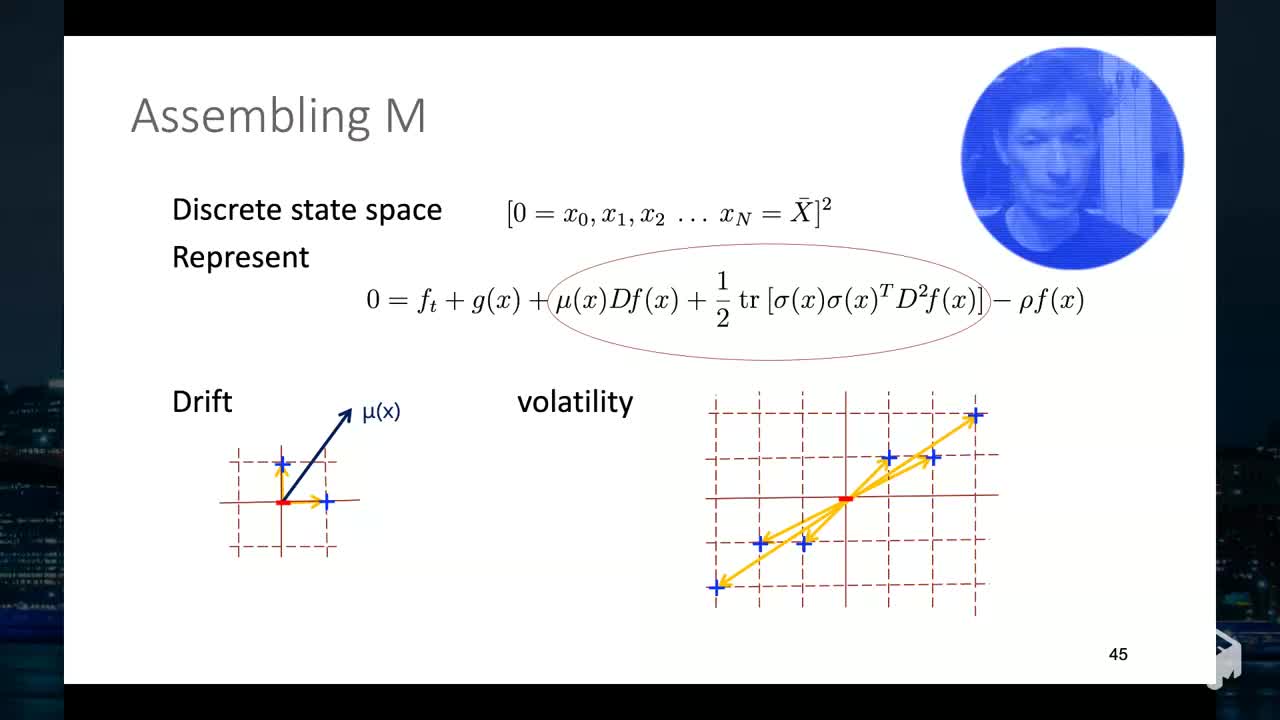

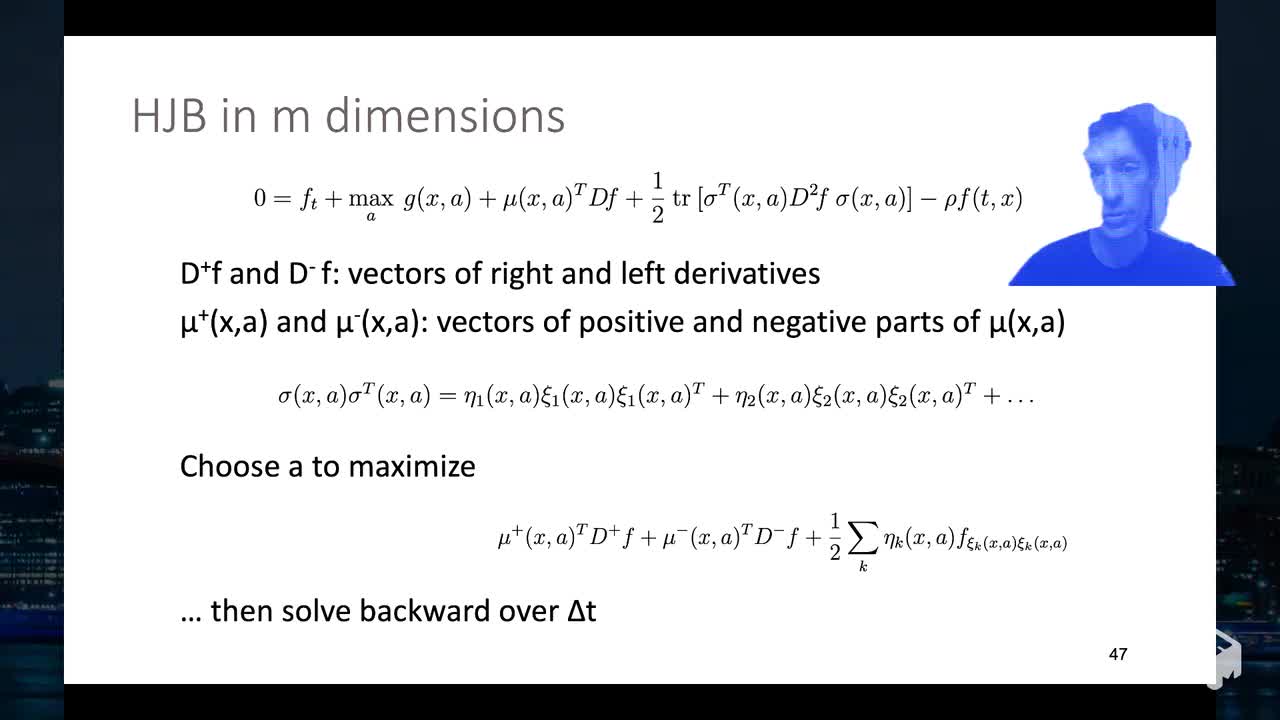

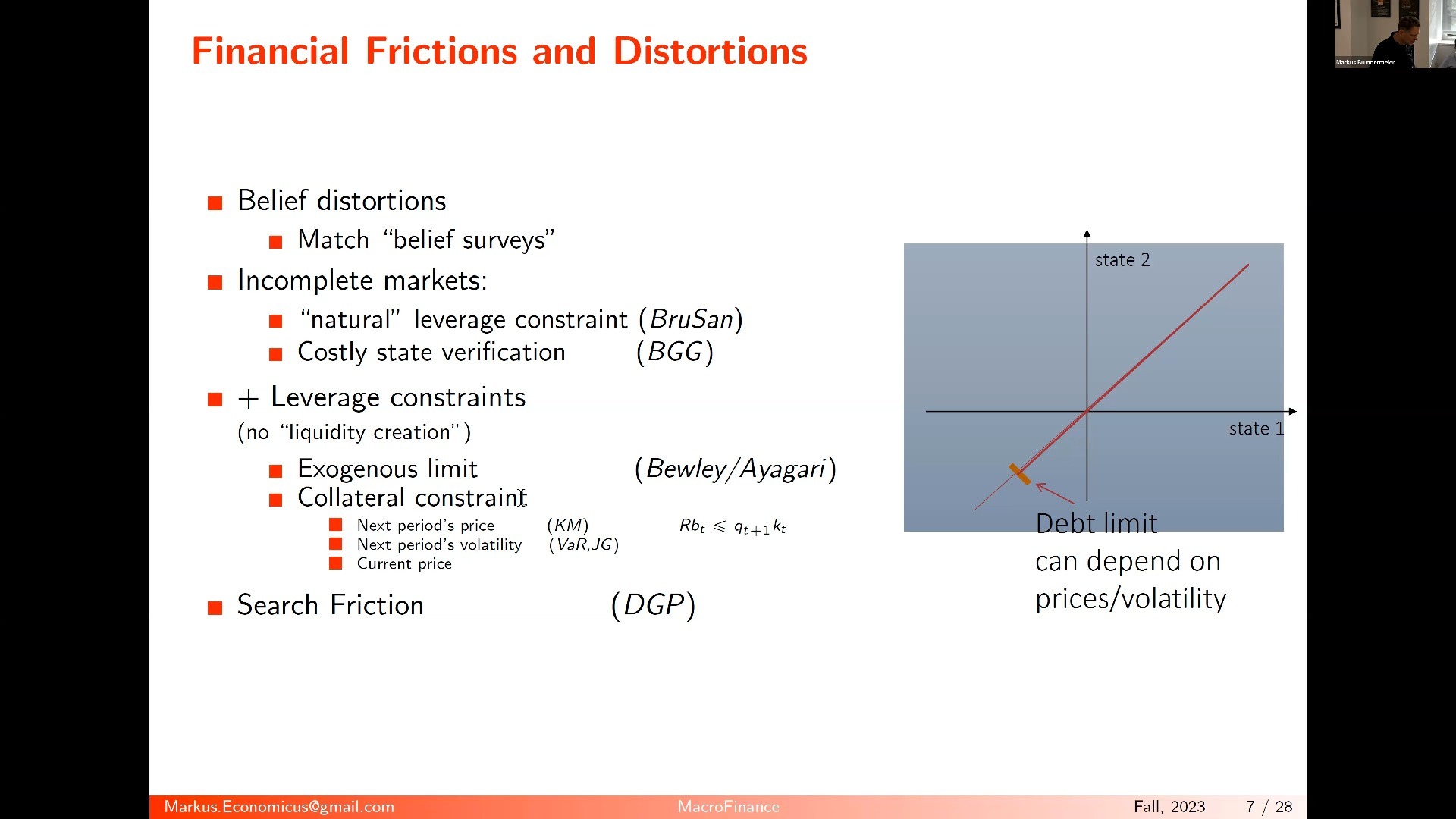

视频选集 1. Why Continuous Time Modeling 2. Continuous Time Stochastic Optimization 3. A Simple Macro-Finance Model with Heterogeneous Agents - 2022 4. Endogenous Risk Dynamics with Log utility 5. Contrasting Financial Frictions 6. CRRA and Epstein-Zin utility, ValueFcn Backwards Iteration 7. Kolmogorov Forward Equation 8. Numerical Methods 8.01 Introduction- General Class of Equations 8.02 Example- Valuation Equation and HJB 8.03 Forward and Backward Equations- HJB, KFE 8.04 Finite Difference Schemes- Key Principles 8.05 Finite Difference Operator and sign of Matrix M 8.06 Explicit Scheme 8.07 Implicit Scheme 8.08 Stationary Value Function in a Single Step 8.09 KFE using Matrix M 8.10 General Class of HJB in One Dimension 8.11 Solving HJB 8.12 Non-monotone Schemes (what can go wrong.) 8.13 Valuation Equation in m Dimensions 8.14 Convex Positive Semidefinite Cone 8.15 Some Geometry Details in Two Dimensions 8.16 The Algorithm for the 2nd-order Term in Two Dimensions 8.17 Assembling M and Solving the Valuation Equation 8.18 Solving HJB Equation in m Dimensions 9. Endogenous Risk Dynamics with Jumps 10. Monetary Store of Value Model with Idiosyncratic Risk 11. Monetary Store of Value Model with Time-varying Idiosyncratic Risk and Safe 12. Medium of Exchange Addition and Contrasting Monetary Theories 13. Unit of Account, Multi-Sector Model, Banking + I Theory of Money 14. Price Rigidities - New Keynesian Elements 15. Welfare and Optimal Policy 16 17. International Monetary System -- 2020 TA Session 02 TA Session 03 TA Session 04 TA Session 05 TA Session 06

点点DDHL的视频 Princeton ECO529: Macro, Money and International Finance 2024 宏观 货币和国际金融 Stanford 2020 Computational Economics By Ken Judd